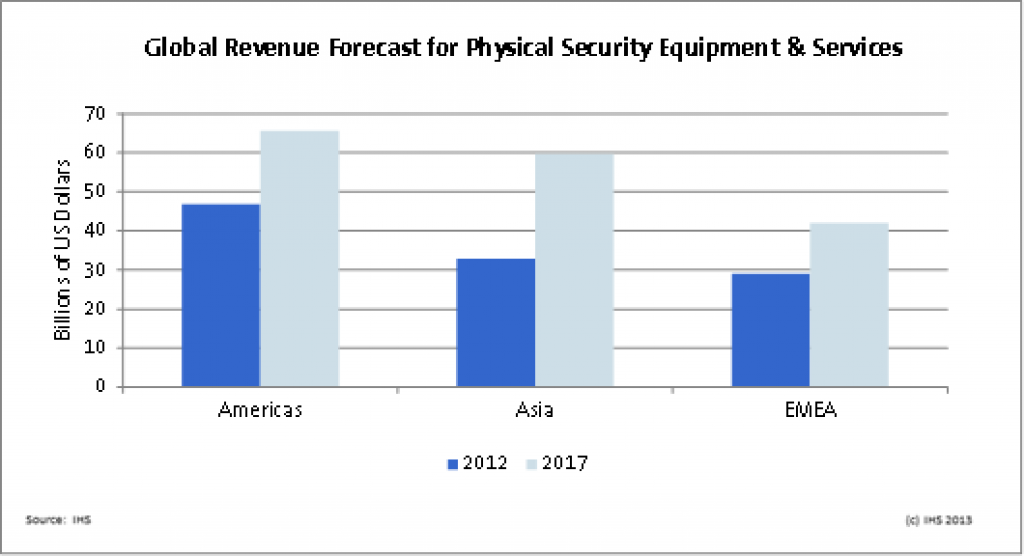

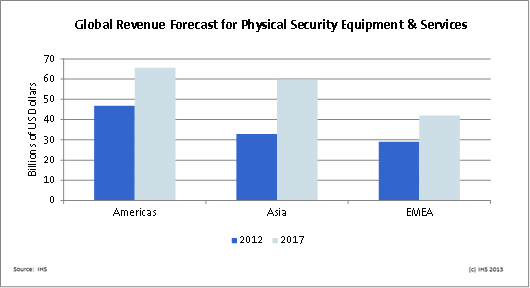

London (Oct.. 3, 2013)—The global industry for physical security equipment and services was worth a massive $110 billion in 2012 with the Americas accounting for more than 40 percent of the overall market, according to the latest research from IHS Inc. (NYSE: IHS), a leading global source of critical information and insight.

Generating $46 billion in revenue last year, North and South America combined made up 41 percent of the worldwide trade for physical security equipment and services. Asia was next with $33 billion, followed by the collective Europe-Middle East-Africa (EMEA) region with $29 billion. Strong growth is predicted in all the markets for the next few years, predicts a finding contained in the new report entitled “Total Physical Security Equipment and Services – 2013.

At its current level, the industry’s annual revenue is double the budget of the U.S. Department of Homeland Security, and is also on a par with the global revenue of giant corporations such as Nissan Motor Co. of Japan, the U.K.’s Tesco or IBM from the United States.

“This is an industry that managed to stay strong during the recession,” said David Green, senior analyst for video surveillance and security services at IHS. “Now with the general improvement in the global economy, we expect total industry revenue to reach $170 billion a year by 2017, even though growth rates will probably peak before then.”

Competition Rules

As the market matures, questions are arising on whether the industry will consolidate. Convention says that as markets age, manufacturers will consolidate until a select few dominate the supply, a theory supported by many within the industry. IHS, however, is not convinced that this will occur because of the huge level of competition and the current fragmentation of the market.

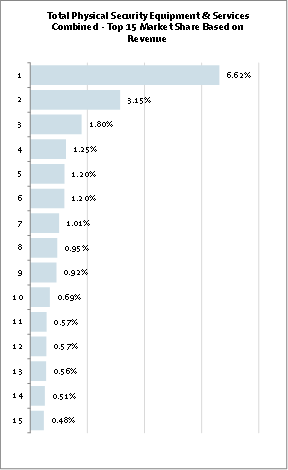

Only two entities, for instance, broke the $2 billion level in annual revenue, with both accounting for a combined market share of 10 percent, as shown in the attached figure. Behind them, only five other companies possess a market share of 1 percent or higher. In fact, the Top 15 together only just managed a market share of just above 20 percent, with the remainder of the market—more than 78 percent—up for grabs among thousands of other companies.

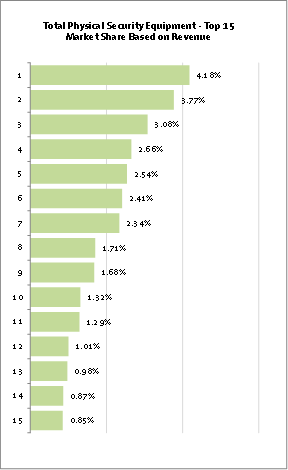

Focusing in to the Equipment market shows a similar story, with a very shallow curve to the market share table. In all, about 40 players in the space achieved revenue in excess of $100 million a year in 2012.

“It’s extremely competitive in every vertical, product and region,” Green explained. “You have several companies that are offering virtually the same product in specification and price, yet the highly personal nature of security sales means that each company can claim its own little niche within the market.”

With the split of Tyco International — one of the largest companies represented in the 2012 data — into ADT, Tyco and Pentair Ltd as separate publicly traded companies, the service market is also set to become even more fragmented in the near-term future.

Is Consolidation Inevitable?

All this means that consolidation of the market may not be as inevitable as one might expect. “True, mergers and acquisitions in the physical security market are inevitable and will happen, especially on the product side of things, but not with the impact you might see in other markets,” noted Green.

For a company to make significant moves up the market share table, it would realistically need the combined share of five or more existing manufacturers. “That’s just not going to happen overnight — this is not an industry where one acquisition propels you straight to the top.”

There is still a general expectation that in the long-term future the industry will start to become dominated by a select few, but it will be a much slower process than traditional market economy studies predict.

“Yes, it defies accepted market logic to some extent,” Green concluded. “But then at $110 billion and beating the recession, it’s hardly a typical industry anyway.”

The IHS report “Total Physical Security Equipment & Services – 2013” combines annual product revenues for the following equipment types: Video Surveillance, Access Control, Intruder Alarms, Perimeter Security, Entrance Control (Pedestrian & Vehicle), Consumer Video Surveillance, Thermal Cameras and Wireless Infrastructure; as well as service revenues assigned to: Video Surveillance as a Service (VSaaS), Access Control as a Service (ACaaS), Remote Monitoring Services and Security Systems Integration. Click here to find out more about the research.

For more information, please contact:

Jonathan Cassell

Senior Manager, Editorial

[email protected]

Direct: + 1 408 654 1714

Mobile: + 408 921 3754

Or

IHS Media Relations

[email protected]

+1 303 305 8021

Or

David Green

Senior Analyst

[email protected]

+44 (0) 1933 40 22 55

About IHS (www.ihs.com)

IHS (NYSE: IHS) is the leading source of information, insight and analytics in critical areas that shape today’s business landscape. Businesses and governments in more than 165 countries around the globe rely on the comprehensive content, expert independent analysis and flexible delivery methods of IHS to make high-impact decisions and develop strategies with speed and confidence. IHS has been in business since 1959 and became a publicly traded company on the New York Stock Exchange in 2005. Headquartered in Englewood, Colorado, USA, IHS is committed to sustainable, profitable growth and employs more than 8,000 people in 31 countries around the world.