This market research report was originally published at the Yole Group’s website. It is reprinted here with the permission of the Yole Group.

At the core of electrification and ADAS lies the semiconductor technologies.

OUTLINE

-

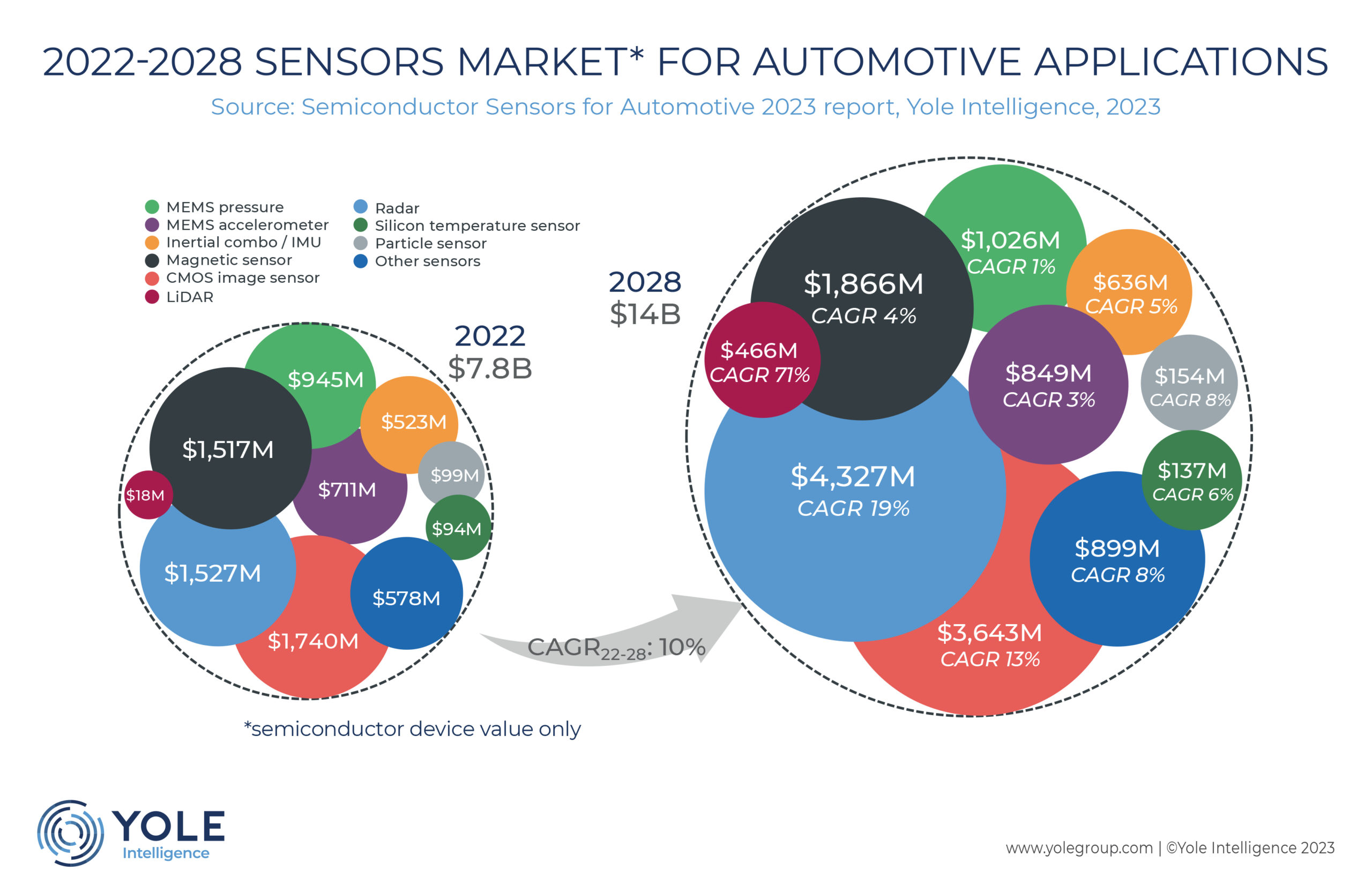

The automotive semiconductor sensor market is expected to reach US$14 billion in 2028, with a 10% CAGR 22-28.

-

Electrification and ADAS & safety remain the main drivers that will impact sensor manufacturers growth or diminishing, depending on their market positioning.

-

Semiconductors sensors in automotive are expected to evolve strongly in all car domains.

-

Along with powertrain ADAS & Safety, the User Experience domain will witness a 10% CAGR22-28 as cars are becoming the third living space, with an increasing number of applications related to comfort and entertainment.

Sensing techniques continue to proliferate. Initially meant to optimize the powertrain’s efficiency, growing safety concerns have made some sensors mandatory: ABS , ESC , airbags, etc. Driven by technology and its initial integration into high-end cars, innovation has diffused to mid to low-end models over the years, giving birth to a multi-billion-unit industry.

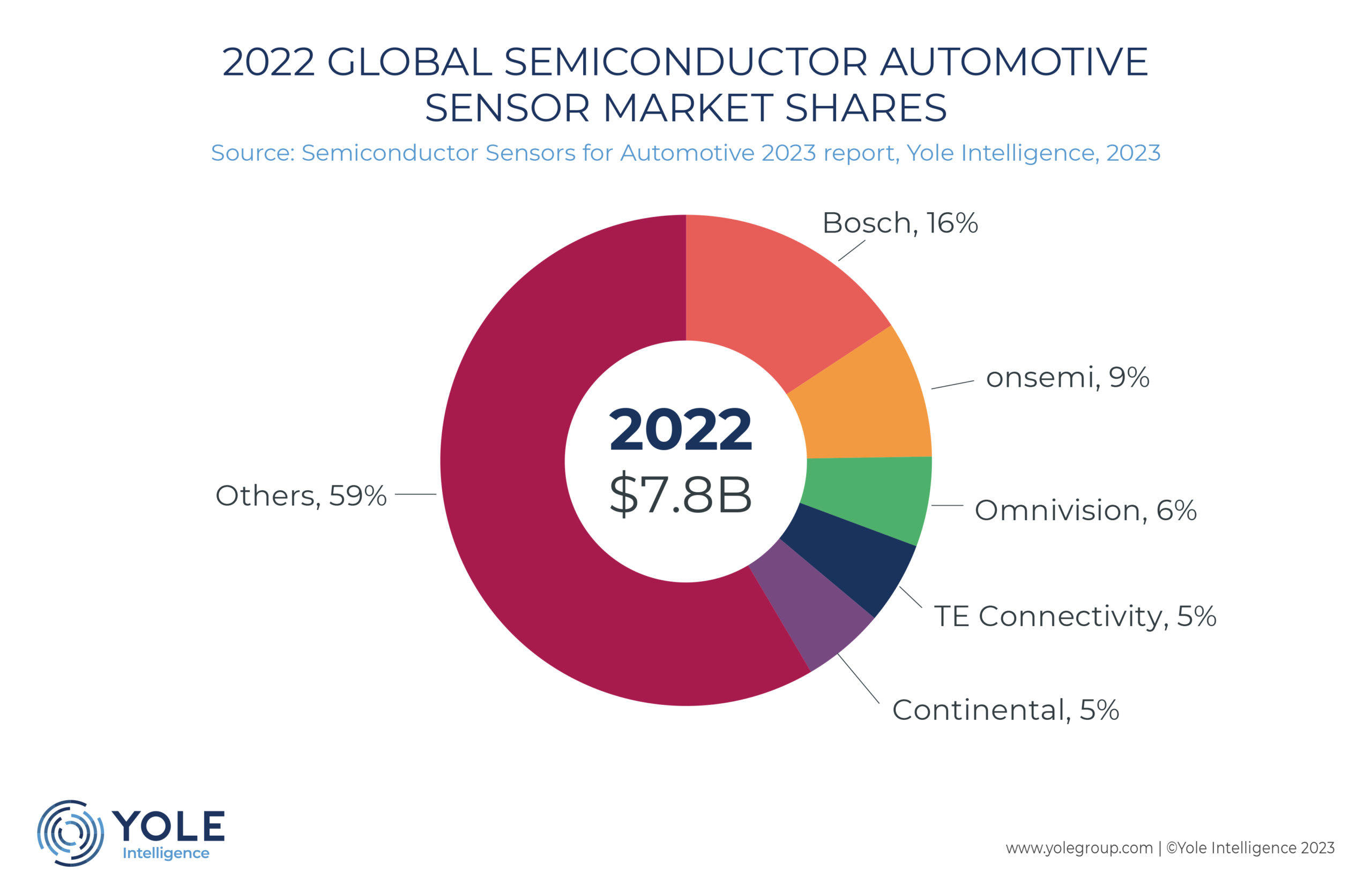

“5.4 billion sensors for the automotive market were shipped in 2022 globally, generating US$7.8 billion in revenue. And with a strong 10% revenue CAGR between 2022 and 2028, we expect it will grow to US$14 billion in 2028 with 8.3 billion sensors shipped worldwide.”

Pierrick Boulay

Senior Technology and Market Analyst, Photonics and Sensing Division, Yole Intelligence (part of the Yole Group)

During the next few years, the automotive industry is expected to go through a massive transformation in all four car domains:

- Powertrain: the automotive industry is transitioning from cars based on ICE , which represented 93% of the production in 2018, to electrified cars, which are expected to represent 37% of the production in 2028. In terms of sensors, the powertrain & EM domain will be worth more than US$1.5 billion by 2028, growing with a 2% CAGR22-28. In the long term, the electrification of cars will induce critical changes in the sensor landscape by giving birth to new applications while removing others.

- ADAS & safety: from enhanced safety to autonomous driving, cars are becoming more intelligent. Cameras, LiDAR s, radars, and so on are helping cars take action based on an understanding of their environment. Revenue from the ADAS & safety segment is by far the largest of all segments, with US$8 billion expected to be generated by 2028.

- User experience: for product differentiation, the number of functionalities has been increased, and the in-cabin comfort improved over the years. Fostered by autonomous driving (so more entertainment will be needed for the driver and the passengers), this domain will experience a nice 10% CAGR22-28, reaching more than US$2.9 billion in 2028.

- Body & chassis: to improve the safety of passengers, to send valuable data to the ADAS computing unit, or even to remove hydraulic components of the car, the global sensorization of cars is driving the sensor volume to grow at a 7% CAGR22-28. In terms of revenue, Yole Intelligence expects almost US$1.4 billion to be generated in 2028.

ADAS and autonomous driving, electrification, and global sensorization are expected to vigorously shake up the sensors for the automotive industry in the coming years. As a result, a significant restructuring of this industry and its supply chain is expected. Hence, the time to make a strategic business plan and work with the right partners is now.

“Even though electrification and ADAS & safety are the main drivers, technology is expected to evolve in all car domains.”

Pierre Delbos

Technology and Market Analyst, Photonics and Sensing Division, Yole Intelligence (part of the Yole Group)

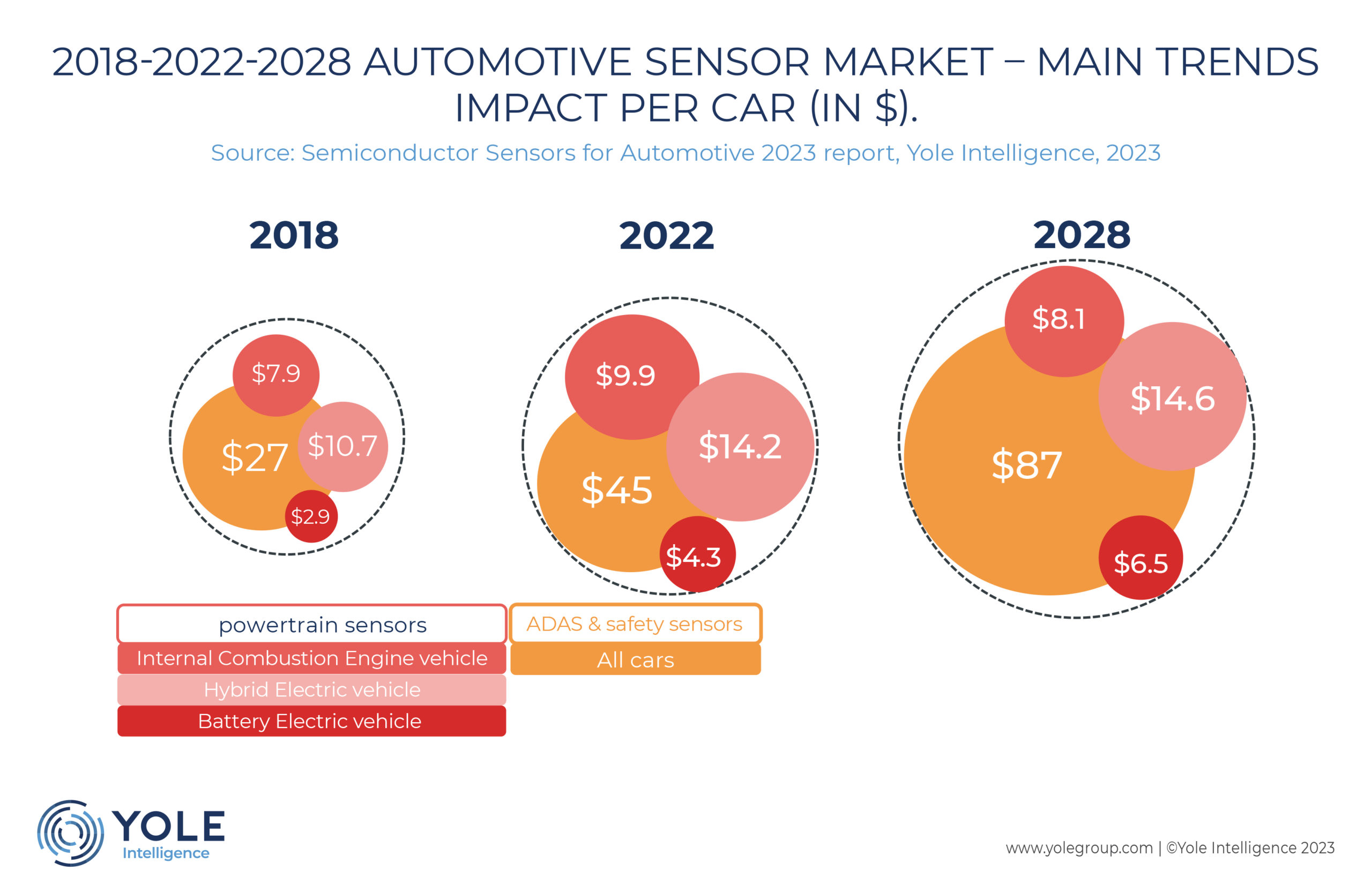

- Powertrain: with the overall trend to increase battery capacities and develop 800V batteries, the penetration of magnetic (isolated) technologies ramps up in the coming years for current sensing in the OBC , DC/DC , inverters, and power modules. Indeed, shunt sensors are cheap and very accurate but lack galvanic isolation. Therefore, Yole Intelligence’s analysts expect a change in technology from shunt sensors to magnetic sensors in the coming years. Also, the battery must be kept in the optimal temperature range to ensure better performance, comply with safety requirements, and provide a longer life. To do so, magnetic sensors are positioned on thermal valves to precisely control the injection of cooling/heating fluids. Therefore, the sensor content per BEV will grow from US$4.3 in 2022 to US$6.5 in 2028. (These figures include sensors dedicated to the BEV powertrain).

- ADAS & safety: CMOS image sensors are expected to evolve to increase the number of frames per second, the dynamic range, and temperature resistance. This is not a significant technological change but will answer the need of Tier-1s and OEMs. Radar sensors are continuously evolving, and the next significant change is related to the introduction of 4D imaging radar to achieve a below 1° angular resolution, which is impossible with conventional 3D radar. This evolution is linked to the development of new MIMO technics enabling an increase of the virtual aperture while keeping a reasonable physical size.

- LiDARs are quite young compared to image sensors and radar, and their technology is changing rapidly. The main improvement is related to the distance LiDAR can sense. For this, different types of lasers can be used, EEL s, VCSEL s, or fiber. But the main improvement is related to the receiver, where the technology is transitioning from avalanche photodiodes to SPAD s and SiPM s that are much more sensitive. This will lead the sensors for ADAS & safety content per car to grow from US$45 in 2022 to US$87 in 2028.

- User experience: No real breakthrough technology is expected, explains Yole Intelligence in its new report. But more sensors will be implemented for comfort applications. MEMS sensors will be used to improve phone calls and noise-canceling applications. Capacitive sensors will replace physical buttons, and radar will be used for occupant monitoring. Moreover, environmental sensors will be critical devices to improve the in-cabin air quality.

- Body & chassis: The main innovation is linked to the development of brake and drive-by-wire technologies to remove hydraulic components of the car. Here, magnetic sensors are crucial for pedal position sensing and motor position monitoring. In addition, Yole Intelligence expects a slow adoption of smart TPMS modules not only measuring tire pressure but also giving essential information on tire quality, weather conditions, and the car’s load to the main processing unit. Other applications could be linked to monitor the driver’s position on the seat and adjust its position slightly over time during long journeys.

Yole Intelligence’s Sensing & Actuating team invites you to follow the automotive technologies, related systems, modules, devices, applications, and markets on www.yolegroup.com.

In this regard, do not miss Analyst Thursday – Automotive Electrification on September 7th, 2023, more information coming soon.

Stay tuned!

Acronyms

- CAGR : Compound Annual Growth Rate

- ADAS : Advanced Driver-Assistance System

- ABS : Anti-lock braking systems

- ESC : Electronic Stability Control

- ICE : Internal Combustion Engines

- EM : Electric Mobility

- LiDAR : Light Detection and Ranging

- OBC : Onboard Charger

- DC/DC : Direct Current Convertor

- BEV : Battery Electric Vehicle

- MIMO : Multiple-Input And Multiple-Output

- EEL : Edge Emitting Laser

- VCSEL : Vertical-Cavity Surface-Emitting Laser

- SPAD : Single-Photon Avalanche Diode

- SiPM : Silicon Photomultiplier

- TPMS : Tire Pressure Monitoring System