This market research report was originally published at the Yole Group’s website. It is reprinted here with the permission of the Yole Group.

From automotive to consumer, radar adoption is experiencing a surge driven by regulation and innovation.

OUTLINE

-

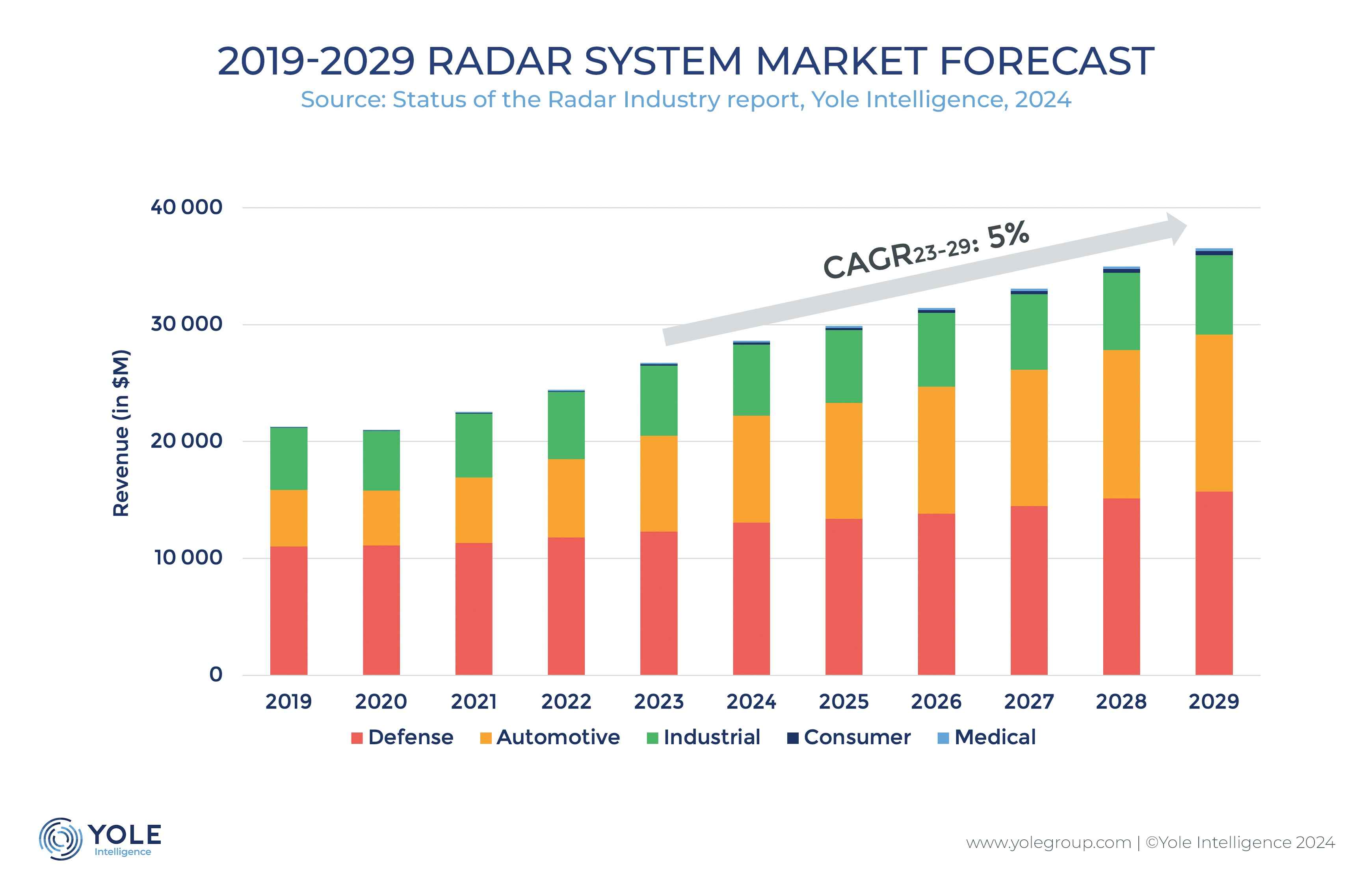

The radar module market is projected to reach close to US$36.5 billion by 2029, exhibiting a 5% CAGR from the US$26.7 billion in revenue recorded in 2023.

-

Automotive sector: expected to expand at an annual rate of 9%, from its 2023 value of US$8.2 billion, it is forecasted to reach US$13.5 billion by 2029.

-

Industrial sector: despite being worth US$6 billion in 2023, the industrial radar market is projected to experience modest annual growth, with a rate of 2%, to US6.8 billion by 2029.

-

Defense, security and aerospace sector: It will generate US$12.3 billion in 2023, but its growth potential is limited, with an anticipated CAGR 23-29 of 4%, to reach US$15.7 billion in 2029.

-

Consumer sector: the approval by the FCC to allow 60GHz radars for mobile applications could propel the consumer radar market from US$0.11 billion in 2023 to US$0.35 billion in 2029.

-

Medical sector: The medical radar market is anticipated to witness a growth rate of 12% CAGR, from US$0.12 billion in 2023 to US$0.25 billion in 2029.

-

-

NXP, Infineon Technologies, Texas Instrument… Growing competition is compelling major chipmakers to reassess their strategies.

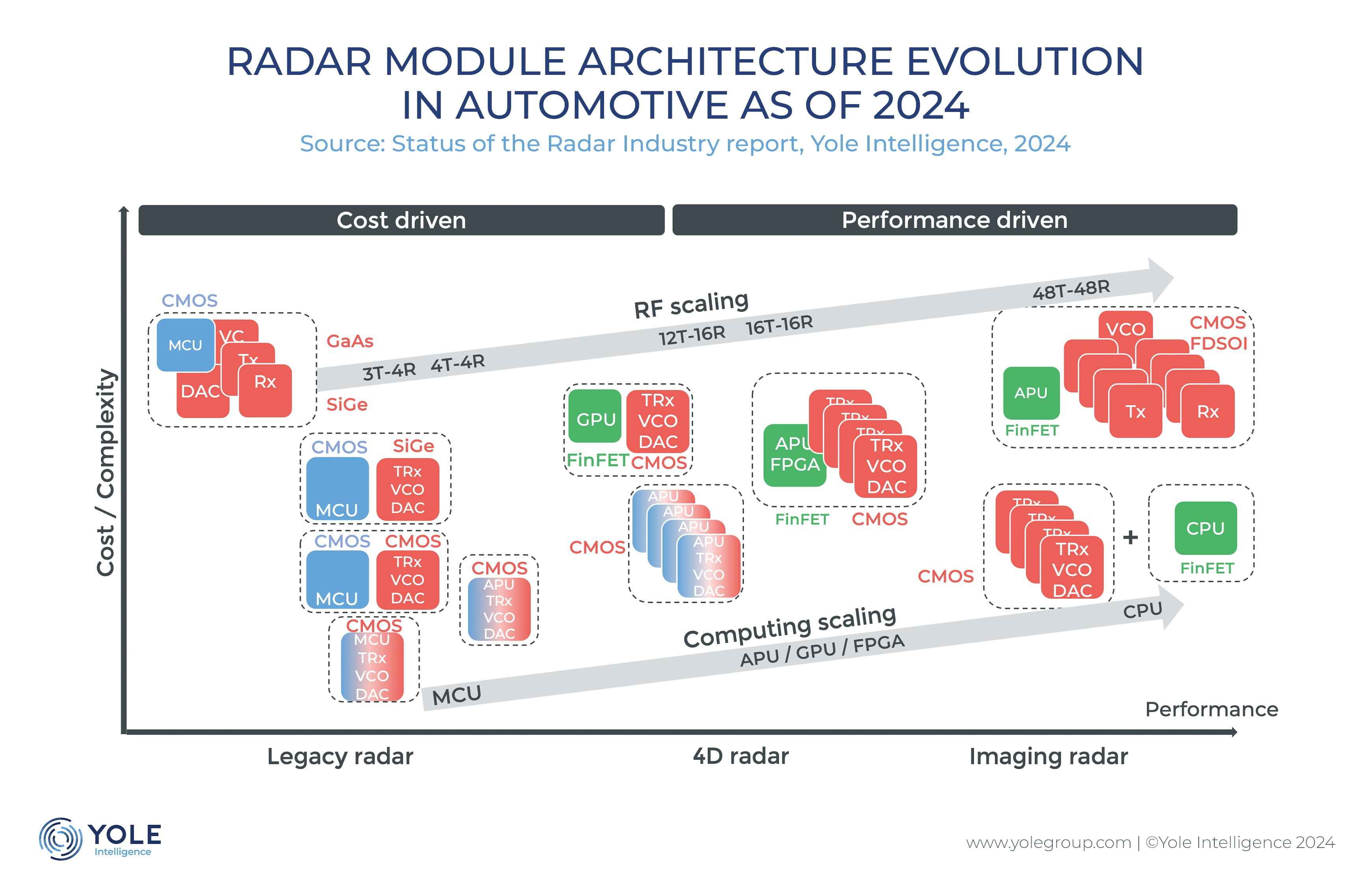

In the ever-evolving field of automotive technology, the transition from GaAs to SiGe and now to CMOS radar modules has been revolutionary. This transition has not only drastically reduced costs but also hints at a future where the price of standard 77GHz radar could drop as low as US$30 by 2030. However, the aspirations extend beyond cost reduction. Indeed, there’s a concerted effort to decrease the average selling price of state-of-the-art 4D imaging radar to align with OEMs’ budget constraints.

“Despite strides in radar technology, current capabilities still lag behind the requirements for fully autonomous driving. Module manufacturers are actively exploring diverse architectural approaches to bridge this disparity, aiming to expand the FOV and enhance angular resolution. This exploration involves strategies such as increasing RF channels, enhancing computing power, or a combination of both to achieve optimal results. It’s a dynamic landscape fostering innovation in pursuit of the ultimate goal of autonomous driving.”

Raphaël da Silva

Technology & Market Analyst, Radio Frequency at Yole Group

Moreover, OEMs are leading a significant transition toward vehicle centralization, anticipated to be fully implemented between 2030 and 2035. This shift anticipates a future where more cost-effective, compact radars with advanced computational capabilities and superior system performance become the norm, paving the way for a truly autonomous driving experience.

Radar usage is also extending beyond its conventional applications, spurred by fresh FCC regulations and advancements in radar technology. This shift isn’t limited to established sectors, such as automotive, industrial, and defense; it’s also penetrating emerging fields like consumer electronics and healthcare. Enhancements in precision, dimensions, affordability, and energy efficiency are aligning radar perfectly with these burgeoning markets, unlocking substantial prospects.

In this context, Yole Group has combined its significant semiconductor expertise and deep knowledge of radio frequency technologies and markets to deliver its annual report, Status of the Radar Industry. This study dives deep into the radar supply chain, the systems that use radar technology, and the latest trends in radar technology at various levels, from entire systems to antennas and devices. It explains the key factors that influence the global radar market and analyzes the competitive landscape in detail.

The radar module market is fiercely competitive, with numerous companies vying for market dominance. This competition spans various sectors, from the crowded automotive radar sector to specialized niches in industrial applications. Consequently, module providers like Continental, Bosch, Aptiv, Smartmicro, InnosenT, are consistently lowering prices to maintain their competitiveness. Recent partnerships among OEMs, Tier 1 suppliers, chipmakers, and antenna manufacturers are gaining traction, highlighting the strategic positioning of each participant.

While the module provider landscape is fragmented, the radar device market is dominated by a select few players,” explains Raphaël da Silva. “These established entities, known for their cross-industry supply, now face fresh competition from diverse players, including consumer electronics companies and OEMs, seeking to enhance their value proposition by developing proprietary chips.”

Recent technological advancements are poised to reshape the market, particularly with the integration of the transceiver and processing functionalities into single radar chips enabled by CMOS technology. This innovation promises cost efficiencies, space optimization, and supply chain streamlining for OEMs. Additionally, in the automotive industry, companies are preparing for a transformative phase in E/E architecture, which will fundamentally redefine the roles of industry participants.

Acronyms

- CAGR : Compound Annual Growth Rate

- GaAs : Gallium Arsenide

- SiGe : Silicon–Germanium

- CMOS : Complementary Metal-Oxide-Semiconductor

- OEM : Original Equipment Manufacturer

- FOV : Field of View

- E/E : Electrical/Electronic

Yole Group’s radio frequency team invites you to follow the technologies, related devices, applications, and markets on www.yolegroup.com.

In this regard, do not miss ENMORE AUTOMOTIVE CONFERENCE – EAC 2024 on June 21-22 in Suzhou, China. Interested in an onsite meeting with our experts Raphael da Silva and Pierrick Boulay, Senior Technology & Market Analyst, Automotive Semiconductors? Please send us your request at [email protected].

Stay tuned!